Insights & Opinions

The long term impact of COVID-19 on the payments industry

Tue, 07 Apr 2020

Our society has changed, also in the way we pay. We avoid cash and we embrace digital solutions. Contactless is promoted as the ‘healthier alternative’ to cash. Small nuance on this though: a BIS (Bank of International Settlement) bulletin shows that “scientific evidence suggests that the probability of transmission via banknotes is low when compared with other frequently-touched objects, such as credit card terminals or PIN pads.”

But OK, perception is everything, right?

And so Belgium will increase its limits for contactless payments to €50 for a transaction, and the cumulative amount will be increased to €100, just like Luxembourg and the Netherlands did.

The current crisis is forcing people to go digital, whether they like it or not. It will not only impact the way we consume today, but also the way we consume tomorrow.

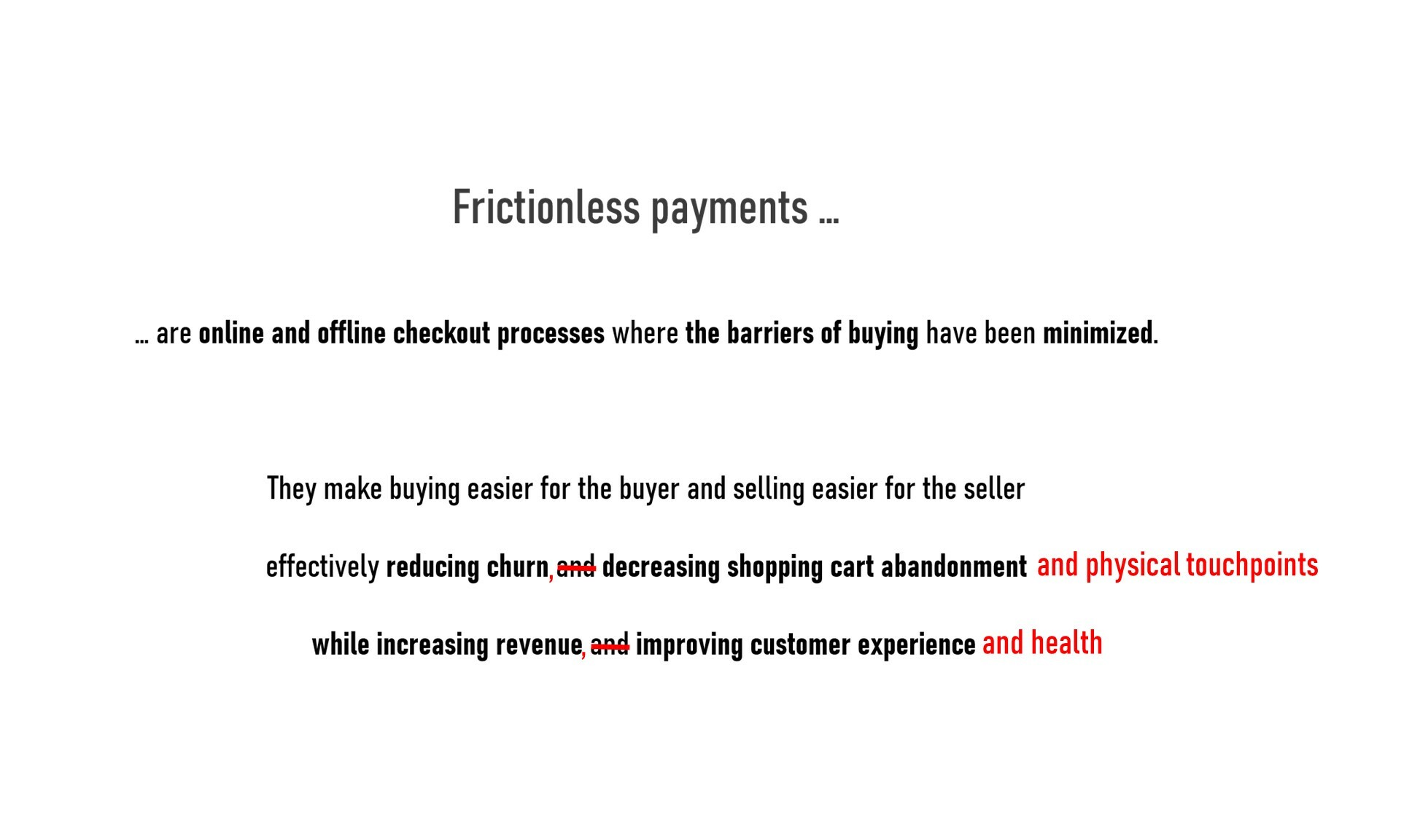

Frictionless payments suddenly got a new definition:

Marc Raisière, CEO of Belfius, is already looking at the future, also the one of payments: “Inserting your card into a card reader and tapping a PIN-code will no longer be required in the future. You will pay by entering a code on your smartphone”.

We will be more flexible in adapting to new payment solutions. Hygiene suddenly becomes an additional characteristic to determine which solution to use.

A few months ago I blogged about the “5 levels of intrusiveness”. I claimed that in Benelux we are not ready yet for too much facial recognition and other innovations that have an impact on our privacy. I may have to take those words back. Will our society be more open towards more intrusive payment methods, if it helps them to stay healthy?

Hard to say today how much of an impact COVID-19 will have on the way we pay. But it is clear that there will be an impact and a big one!

From contactless to no contact

COVID-19 induces a forced behavioural change. Even after the payments behavioural change, people will keep adapting to convenient ways to exchange money. Convenience suddenly became a matter of reducing friction, especially by reducing touchpoints with external machines or contact between one human and another.

Solutions like Payconiq or Carpay Diem already provide this kind of services. They allow you to authenticate on your own device, with the external touchpoints are out of the equation. Open Banking Marketplaces, like KBC will further build on this.

Remember Karin Van Hoecke, General Manager Digital Transformation at KBC Bank & Verzekeringen in her Open Banking Interview:

“The more you can create this ultimate laziness for the customer, without the need to really be there, the more they will appreciate you. In creating this kind of experience you also achieve the new loyalty. That is certainly a big trend.

If we as a bank can simplify the process of parking, or paying at a gas station, account opening, then customers will come back. For small companies, the ‘all-in-one app’ strategy still makes sense. Of course, you need to tweak it every once and a while.”

Health is an additional argument to speed up this evolution.

We are moving from cash to less cash to contactless to no contact at all. Depending on how the current crisis will affect our perception on privacy the payments industry will be very interesting to follow up.

Biometrics

Biometrics isn’t anything new. Biometrics exists for decades already, all over the world and in all kind of use cases. In Belgium though, the rise of biometric solutions is pretty recent. Because biometrics touches the essence of our identity, it wasn’t perceived as a trusted technology.

As the technology matured, our mindset did so too. We started to use it to unlock our phone, our PC. Later we started using it for minor mobile banking solutions, and with the success of Belgian Mobile ID, we use our biometric identity for authentication, for document signing and for executing higher value transactions.

Today’s technology allows for biometric authentication on our device. The merchant doesn’t need our fingerprint or face image, he simply needs a validated transaction. The future will provide more and better-integrated solutions, and with respect to privacy.

Suppose that COVID-19 would make people less sensitive to privacy because apps that are used in China provide more freedom in exchange for constant monitoring. In that case, it would be a small step to facial recognition in a store or at an ATM: no friction, no touchpoints.

Voice recognition is another battlefield for payment innovations. Our interview with Daniel Van Delft, Country Manager Visa Netherlands of almost a year ago showed the huge potential:

“It will take a while before this kind of innovation becomes the norm, but it is around us already, and it will be big in the future. Voice-commerce will be another variety where we see the future going”.

Both Visa and Mastercard patented their proper sounds for validated payments.

There is still a lot of work in this field. Marc Beresford of Edgar Dunn: “The new Strong Customer Authentication (SCA) requirements could pose a challenge for merchants enabling voice payments (but not limited to this payment method) in the European Union. Indeed, their customers’ payments could be declined due to stricter authentication measures that will be enforced by 31 December 2020 (new migration deadline set by the European Banking Authority (EBA)). While harmonisation in Europe remains to be a challenge for SCA, voice-commerce may be put on mute for some time until security can be adequately addressed in a fully SCA compliant environment.”

Time for payments infrastructure investments

China is using the circumstances to invest massively, not in (rail)road and other physical infrastructures, but in 5G and other technologies. Sven Agten wrote an opinion about this on April 3: “China is using the corona crisis as an opportunity to accelerate and extend its digital strategy. This creates huge opportunities for companies that are active in these sectors and at the same time it leads to more control over technology and the nation as a whole.”

Europe is still figuring out how to boost the economy post COVID-19. At the moment it is everyone on its own. Local shops that were mono physical are forced today to set up a webshop. Luckily the technology allows them to set up a webshop in just a few days, or even hours to start promoting and selling their products online, including the necessary payment tools: card payments, often dominated by the international schemes like Mastercard, Visa, PayPal. These are embedded payment tools in the standard webshop packages with a low fixed cost, but often a higher variable cost.

Most of these webshops will not go ‘back to normal’, they will not close again once they can open their physical stores. Some will take advantage of the digital experience to close their physical store, others will to hybrid: webshop + physical shop or take away, for all kind of goods. Some will use traditional platforms (Amazon, Facebook,…); others will brand their products locally through their website and platforms.

Recession is there and depression is looming. If depression pops up, we will have increasingly more people working on a day-to-day basis, a push towards an intensified gig-economy, so to say. These people look for instant gratification for the delivered goods or services and in the worst case, in some countries, this could become a matter of life and death.

At the beginning of January, I raised the hope for 2020:

Technology is a means to an end. Banks and fintech should soon realise that the end should be the customer and society. This mindset is growing. A more open environment, sufficiently secured, will drive innovation in the coming years. We see it in the evaluations of PSD2: there is an understanding that for Europe this was just the beginning. In regions that are just at the beginning of Open Banking, they learned from this and they are already thinking further.

Financial services are at the heart of our economy and our society. They can make or break societal ambitions. A positive and creative reflection on how banks can cope with this in the future will also determine the industry’s reputation.

Instant payments and PSD2 offer a few foundations to help the local small businesses reduce their transactions costs in the future. More importantly: it gives them instant cash, which is in time of crisis even more important than saving a bit on the variable costs.

Why not take advantage of this in the payments industry? EPI (European Payments Infrastructure) is a huge investment, but in the current context, it seems to be increasingly more relevant. Besides these infrastructural investments and the related employment, it will make Europe less dependent of global players, it will ignite new innovations and it will generate a new wave of investment to embed the new payment solution in the European economy. Most importantly: it puts Europe back in the lead in how to move their local trade forward.