Insights & Opinions

The future of banking is for the nimble and niche players

Sat, 16 Mar 2019

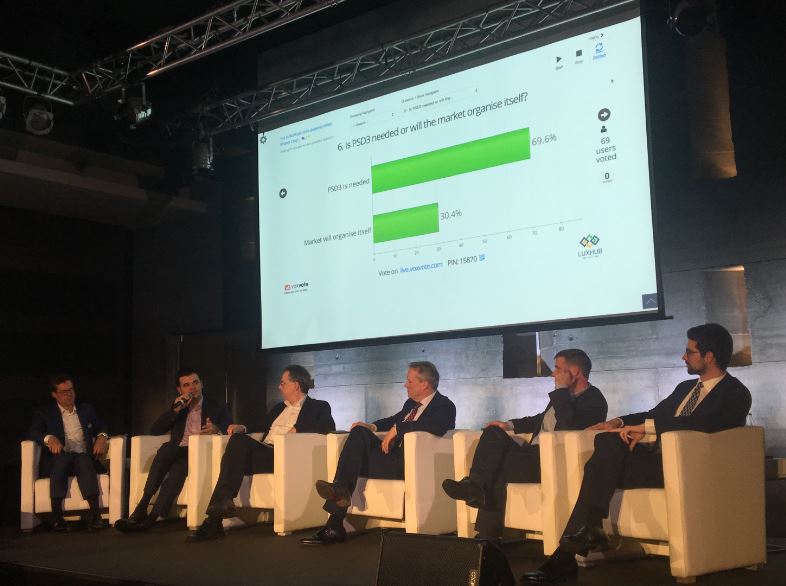

March 14 was the official deadline for financial institutions to have their API platforms ready for PSD2. I had the pleasure to celebrate this at LUXHUB’s Europen Open Banking Panel, on March 13 with a great list of key people of the industry. A day later, I was invited by Capco at their innovation conference, which was titled “Neobanks, fintechs and banks: the changing landscape”.

Another day later there was the announcement of BNP Paribas Fortis that they would close 4 out of 10 branches in the next 3 years.

Very interesting 3 days in the world of banking…

PSD3 will come

Key take-away one: PSD3 will come. That is not my statement, it comes straight from Gijs Boudewijn, who said it in Luxembourg and Reinout Temmerman, who said it in Brussels. When they come up with this kind of statements, you can be confident it will happen. Gijs Boudewijn is Chair of Payments Systems Committee at The European Banking Federation, and Reinout Temmerman is Oversight Analyst at the National Bank of Belgium, specialised in Payments Services Directive and E-money Directive.

They understand that PSD2 still has its weaknesses and that quite a lot of elements that are open for interpretation. Times change, but regulation often lags behind. The spirit of PSD2 was created pretty close to the time the app store was launched.

LUXHUB

LUXHUB

The limit to current accounts is an element of discussion. In the very beginning the regulator assumed Payment Initiation was the key element that would drive innovation. Today they encounter a lot more request for Account Information services. Data is where value can be created, not the payments themselves.

As a consequence, PSD2 should be extended to a lot more accounts to make sure that Fintechs can deliver proper services to their customers through AISP. This debate is especially relevant in Luxembourg, with the high concentration of family offices and wealth managers. Today Open Banking means almost nothing to them as long as it is limited to PSD2.

Another pain point is RTS: the regulatory technical standards are not yet what they should be for a well-functioning user experience. Ralf Ohlhausen (Executive Adviser at PPRO and Tink) made this very clear. According to him a PSD3 is not really necessary, on condition that there will come an RTS2!

It is clear there is still a lot of work and debate ahead of us to make financial services more flexible, more digital and more open!

The future is for the nimble

The times are over when setting up a bank takes 5 years . If you need 5 years to build a bank, it is better to simply give up the plan.

Take the example of Mettle (that is right, Mettle, not metal, like “a person’s ability to cope well with difficulties; spirit and resilience”). Mettle is a standalone digital bank of Royal Bank of Scotland, created in collaboration with 11:FS and Capco. This digital bank was launched in November 2018 in pilot.

That they launched ‘in pilot’ is not a small little detail. This is a complete shift of what banks have always done. Today offering a minimum viable product is seen as an opportunity for more feedback. That is only possible with regular iterations and sprints, and a changed mindset.

In the past (and sometimes even today), banks were organised for 2–4 releases a year and they were afraid of the negative feedback by customers or press.

Today having a pilot is OK. Having a MVP is OK. There is one condition though: communicate it well to your customers. Set the right expectations, make sure they also see it as a pilot!

Mettle is a brand of RBS. This helps them to get the trust of customers. For compliance services for example they count of RBS as well.

They have another back office and they make use of cloud computing. This helps to anticipate faster than RBS, differently and often better on feedback of customers. It differentiates them from the mother ship.

Another interesting detail: they provide banking services, but they are not a bank. They operate as an agent under an e-money licence held by PrePay Solutions, similar to the way Revolut onces started (and still operates). Although is has some disadvantage, it clearly shows a banking licence is not always required for banking services.

Key today is to be flexible and if you can move faster through an e-money licence on the short term, then that is the way to go. The step up to a banking license can be done at a later phase, like Revolut did.

The future is for niche players

Solaris bank offers banking-as-a-service. They can provide any banking service you want, going from the license, to compliance and core banking software etc… Their motto is: you take care of what you are good at, let us take care of what we are good at.

They provide the perfect platform to set up a niche product offering to set up a new business in banking.

This results in new ventures, mainly operated by very good marketeers who know how to brand a product and services. They focus on marketing and sales, Solaris bank helps them with the rest.

A few examples in their portfolio of banks:

Tomorrow: a 100% digital sustainable bank. All the money is invested in sustainable industries, interchange fees of credit cards go to global climate protection projects, they support and promote local, sustainable partners…

Albaraka Türk: a 100% mobile only banking service for Europe’s Muslim community. Is the an interest-free bank with Islamic-friendly services, and even a “Nearest Mosque” locator.

All this is perfectly aligned with the message in Geert Noels latest book as well. He wrote on dangers of “Gigantism”.

Smaller scale companies have more flexibility to deal with change, they have a better contact with the employees and they have a stronger culture.

Banks today mostly come from a long history of mergers of more local players. That is how they were different from each other, it was a regional thing. The need for scale made them grow and today most incumbents offer almost the same services, at almost the same price.

Initiatives like Solaris bank force existing players to reflect on their identity again. Banks that truly find their identity, their niche and that can translate that into a market need, will be the ones that have a chance to survive. It may also be worth looking at my last blog on this topics, where I explain through a few examples that financial services alone are no longer enough to differentiate.

What about the big players?

Big players have possibly most to lose in existing market circumstances. A few will take the lead, and may remain dominant. Others may have difficult times ahead.

That brings us at the news of BNP Paribas Fortis. They launched Didid, and app that helps dreams come true. It is separate app that helps consumers share their dreams, save for dreams and crowdfund for dream. A great story, that deserves a lot of press attention.

A few days later all this gets in the shadow of the struggle with their size. 4 out of 10 branches will be closed over the next 3 years. By 2022 they have work for 2.200 less employees. The reduction in the sales network, further efficiency gains through technology, or simply automation of some jobs should make that possible.

They are exposed to an identity crisis at the moment. Only once they truly understand their value for society, they will be able to find the light again at the end of the tunnel. Only then, it will be possible to announce new great services like Didid without risking the shadow of some negative news.

Please note that this is not only the case for incumbents. The ones who follow Revolut know what I talk about, I guess 😉.